joint product and by product costing for costing students

A joint cost is a cost that benefits more than one product, while a by-product is a product that is a minor result of a production process and which has minor sales. Joint costing or by-product costing are used when a business has a production process from which final products are split off during a later stage of production. The point at which the business can determine the final product is called the split-off point. There may even be several split-off points; at each one, another product can be clearly identified, and is physically split away from the production process, possibly to be further refined into a finished product. If the company has incurred any manufacturing costs prior to the split-off point, it must designate a method for allocating these costs to the final products. If the entity incurs any costs after the split-off point, the costs are likely associated with a specific product, and so can be more readily assigned to them.

Besides the split-off point, there may also be one or more by-products. Given the immateriality of by-product revenues and costs, byproduct accounting tends to be a minor issue.

If a company incurs costs prior to a split-off point, it must allocate them to products, under the dictates of both generally accepted accounting principles and international financial reporting standards. If you were not to allocate these costs to products, then you would have to treat them as period costs, and so would charge them to expense in the current period. This may be an incorrect treatment of the cost if the associated products are not sold until some time in the future, since you would be charging a portion of the product cost to expense before realizing the offsetting sale transaction.

Allocating joint costs does not help management, since the resulting information is based on essentially arbitrary allocations. Consequently, the best allocation method does not have to be especially accurate, but it should be easy to calculate, and be readily defensible if it is reviewed by an auditor.

How to Allocate Joint Costs

There are two common methods for allocating joint costs. One approach allocates costs based on the sales value of the resulting products, while the other is based on the estimated final gross margins of the resulting products. The calculation methods are as follows:

- Allocate based on sales value. Add up all production costs through the split-off point, then determine the sales value of all joint products as of the same split-off point, and then assign the costs based on the sales values. If there are any by-products, do not allocate any costs to them; instead, charge the proceeds from their sale against the cost of goods sold. This is the simpler of the two methods.

- Allocate based on gross margin. Add up the cost of all processing costs that each joint product incurs after the split-off point, and subtract this amount from the total revenue that each product will eventually earn. This approach requires additional cost accumulation work, but may be the only viable alternative if it is not possible to determine the sale price of each product as of the split-off point (as was the case with the preceding calculation method).

Price Formulation for Joint Products and By-Products

The costs allocated to joint products and by-products should have no bearing on the pricing of these products, since the costs have no relationship to the value of the items sold. Prior to the split-off point, all costs incurred are sunk costs, and as such have no bearing on any future decisions – such as the price of a product.

The situation is quite different for any costs incurred from the split-off point onward. Since these costs can be attributed to specific products, you should never set a product price to be at or below the total costs incurred after the split-off point. Otherwise, the company will lose money on every product sold.

If the floor for a product’s price is only the total costs incurred after the split-off point, this brings up the odd scenario of potentially charging prices that are lower than the total cost incurred (including the costs incurred before the split-off point). Clearly, charging such low prices is not a viable alternative over the long term, since a company will continually operate at a loss. This brings up two pricing alternatives:

- Short-term pricing. Over the short term, it may be necessary to allow extremely low product pricing, even near the total of costs incurred after the split-off point, if market prices do not allow pricing to be increased to a long-term sustainable level.

- Long-term pricing. Over the long term, a company must set prices to achieve revenue levels above its total cost of production, or risk bankruptcy.

In short, if a company is unable to set individual product prices sufficiently high to more than offset its production costs, and customers are unwilling to accept higher prices, then it should cancel production – irrespective of how costs are allocated to various joint products and by-products.

The key point to remember about the cost allocations associated with joint products and by-products is that the allocation is simply a formula – it has no bearing on the value of the product to which it assigns a cost. The only reason we use these allocations is to achieve valid cost of goods sold amounts and inventory valuations under the requirements of the various accounting standards.

Problem-1: Market value method for joint cost allocation and reversal cost method for

by products

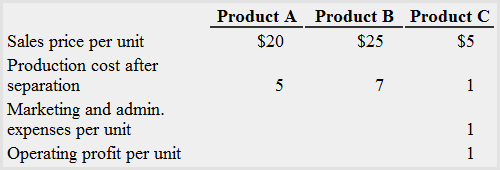

The Abraham Company produces three products – product A, Product B and Product C. Product A and B are the joint products. Product C has a relatively small market value and is therefore treated as a by-product.

During March, 8,000 units of product A, 10,000 units of product B and 2,000 units of product C were processed in refining department. The joint processing cost incurred in the refining department was 204,000.

Some additional data is given below:

The Abraham Company uses market value method to assign cost to product A and product B and reversal cost method to allocate cost to product C.

Required: Allocate joint cost to by-product C and joint product A and B.

Solution

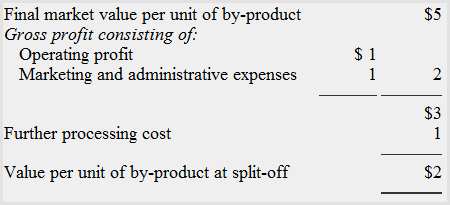

1. Allocation of cost to by-product (i.e., product C):

Value of by-product (i.e., product C) to be credited to joint cost:

Number of units produced × Value per unit of by-product at split-off

= 2,000 units × $2

$4,000

= 2,000 units × $2

$4,000

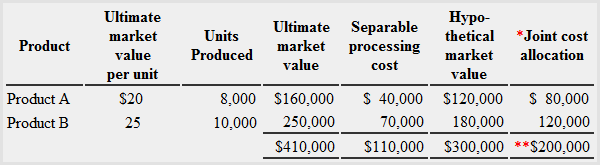

2. Apportionment of cost to joint product A and B:

*Ratio to allocate cost prior to separation

**Total joint cost less value credited to by-product ($204,000 – $4,000 = $200,000)

**Total joint cost less value credited to by-product ($204,000 – $4,000 = $200,000)

Problem-2: Market value at the split-off point

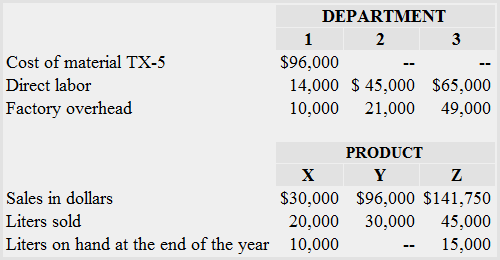

for joint cost allocation

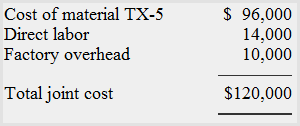

The Roberts Company purchases a material known as TX-5 @ $0.80 per liter. The company has three production departments. In department 1, the material TX-5 splits off into three different products – product X, product Y and product Z. Product X is sold to customers immediately after split-off where as products Y and Z are further processed before they can be sold to customers. Product Y is processed in department 2 and product Z is processed in department 3. The related data for the last year is given below:

There were no material TX-5 and finished goods inventories at the start of the last year. The whole quantity of material TX-5 purchased during the year had been used till the end of the year. No factory overhead variances occurred in the last year. There were no work in process inventories at the start and end of the year.

The Roberts always uses market value at split-off point to allocate joint cost to all of its joint products.

Required:

- For product X, find the market value at split-off of total units produced during the year.

- What is the total joint cost for the last year to be allocated among three products.

- Find the total cost of products X, Y and Z produced during the last year.

- Compute the cost assigned to products X, Y and Z ending inventory.

Solution

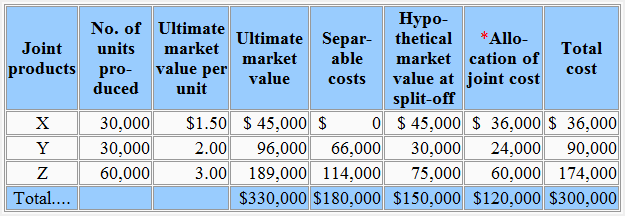

1. Product x – market value at split off point:

Market value per unit × Units produced during the year

= *$1.50 × 30,000 units**

= $45,000

= *$1.50 × 30,000 units**

= $45,000

*$30,000/20,000 units

**20,000 units sold + 10,000 units on hand

**20,000 units sold + 10,000 units on hand

2. Total joint cost to be allocated:

3. Total cost of products X, Y and Z produced during the year:

*Joint cost is 80% of hypothetical market value.

Hypothetical market value is equal to ultimate market value less separable production costs.

4. Cost assigned to product X and Z ending inventory:

Product X:

Cost per unit × Units in ending inventory

= *$1.20 × 10,000 units

= $12,000

= *$1.20 × 10,000 units

= $12,000

*Total cost of product X as per solution to requirement 3/Number of units produced

= $36,000/30,000 units

= $1.20

= $36,000/30,000 units

= $1.20

Product Z:

Cost per unit × Units in ending inventory

= *$2.90 × 15,000 units

= $43,500

= *$2.90 × 15,000 units

= $43,500

*Total cost of product Z as per solution to requirement 3/Number of units produced

= $174,000/60,000 units

= $2.90

= $174,000/60,000 units

= $2.90

Problem-3: joint cost allocation; sell immediately or process further

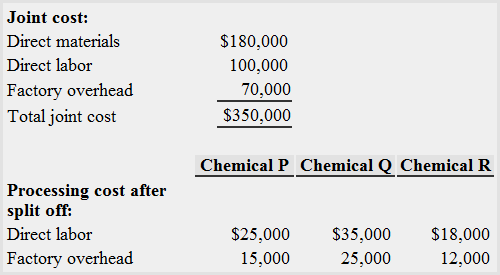

The T&T Company produces three chemicals – chemical P, chemical Q and chemical R. Chemical P is sold for $7 per liter, chemical Q for $5 per liter and chemical R for $8 per liter. During the month of July, 20,000 liters of chemical P, 50,000 liters of chemical Q and 30,000 liters of chemical R were produced and sold.

The cost data for July is given below:

There were no inventories at the start and end of the month. The company uses market value method for allocating joint cost to joint products.

Required:

- Allocate joint cost and compute gross profit for each chemical.

- Decide whether chemical P should be sold at split-off point for $4.50 per liter or processed further and sold for $7 per liter.

Solution

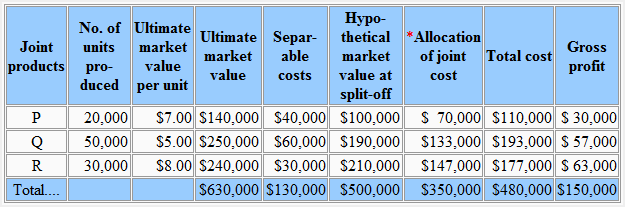

Allocation of joint cost and computation of gross profit:

The joint cost is 70% of the hypothetical market value.

Hypothetical market value is equal to the ultimate market value less processing cost after split-off point.

2. Sell immediately after split-off or process further:

Problem-3 (b):

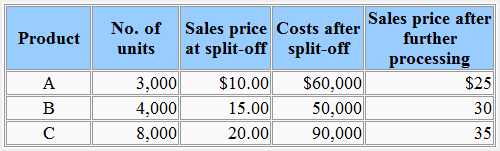

Products A, B and C are produced by incurring a joint cost of $100,000 in a joint production process. All of the three products can be sold at split-off point or processed further and sold at relatively higher prices. You are provided with the following data:

Required: Which product(s) should be sold at split-off point and which product(s) should be further processed after split-off point. All processing costs are variable.

Solution

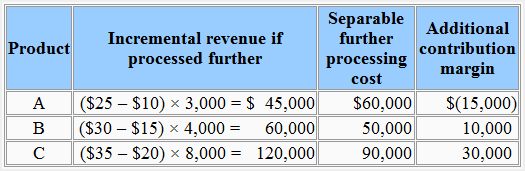

According to above analysis, product A should be sold immediately after split-off point but products B and C should be processed further. If product A is processed further, it gives a negative additional contribution margin which means the further processing of this product would negatively impact the net profit of the firm. In case the products B and C are further processed, their differential revenue becomes more than their differential cost which means an additional contribution margin for these two products. The higher contribution margin would eventually translate into additional profit for the firm.

Comments

Post a Comment